Skip to content

Skip to content

Outlook

This week is dedicated to inflation. Germany’s data are due tomorrow, while the US PCE and the eurozone’s numbers are due on Friday.

Expectations for the eurozone are that the ECB will cut in June and that the core rate will stay at 2.7% (with the headline going up to 2.5% from 2.4%). This is being referred to as a “hawkish cut,” one of those oxymoronic words.

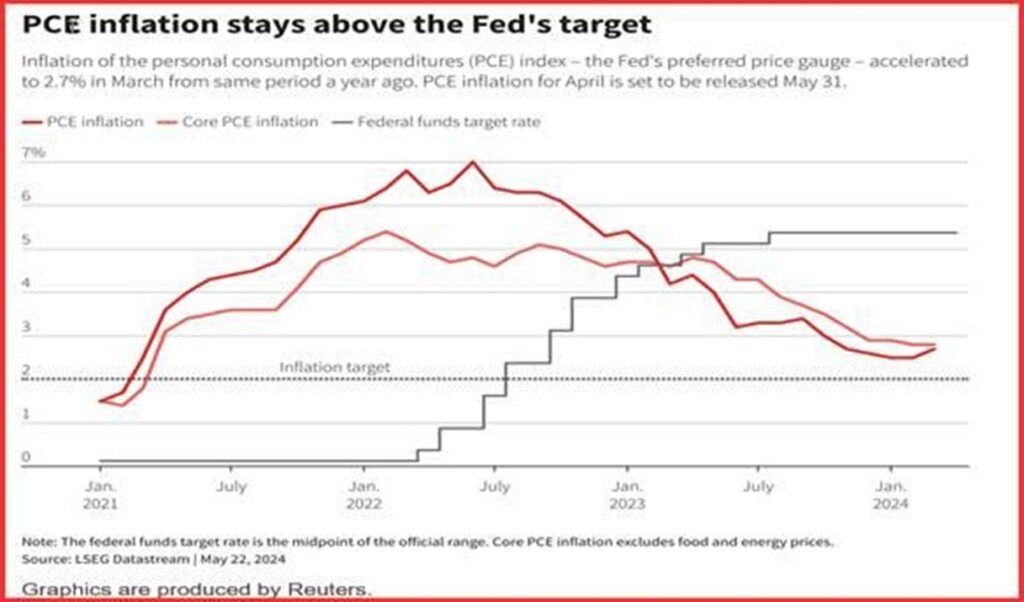

The flash PMI last week in the US dispelled the pessimistic predictions, and core PCE is currently estimated at 0.2%, down from 0.3%, or 2.7%, down from 2.8%, the previous time. At 2.7% y/y, the headline CPI is predicted to stay stable. This is supported by the Cleveland Fed’s Nowcast, which puts the headline and core at 2.7%. This is hardly the kind of disinflation that would be desired or required to destroy the currency.

The dollar’s upward correction abruptly stopped on the Friday before the US holiday, reportedly due to the durables and University of Michigan survey findings that indicated the economy was slowing and becoming less inflationary, and that the Fed was poised to resume cutting rates.

Poppycock. Policy decisions about PMIs, durables, or surveys are not made by the Fed. Their contribution to the ultimate decision, which is based on employment and inflation, is negligible. Not employment and inflation trends, but the real numbers. Naturally, traders are free to over-extrapolate and confuse one thing for another, but this type of whipsawing makes them look even more foolish than they already are. It doesn’t assist to point out that it’s a short-covering rush; panic is still present.

The Fed’s December 2017 comments about the possibility of rate cuts were predicated on the appearance of a disinflationary trend. However, it proved to be a mistake as the first quarter’s three months showed a halting disinflation trend, in addition to the markets going crazy and beginning to count no fewer than six cuts this year.

A fatal reversal is not the same as stalling. However, the markets once more determined that they should consider a raise if FOMC members were able to (at least for a week or two). The market and the Fed are unaware that trend-following does not imply straight lines. They also don’t understand that trends might be influenced by sporadic causes and side effects.

One significant example of this is the profound impact of pandemic and demography on the labor market, particularly in the United States. They have also had an impact on the property market, as a large number of Baby Boomers are reluctant to sell their houses, even at high prices, due to the high cost, high mortgage rates, and poor construction quality of retirement homes. Then there are the homeowners in the upper middle class who acquired a second property and significantly decreased the inventory.

In the US, the epidemic has arguably had the largest impact; in other countries, people have experienced real war in their backyards and have accepted COVID more easily. Similar to the Great Depression, the post-Depression economic behavior took politicians and economists by surprise. They attributed the massive recovery to the GI Bill, Levitt villages, and unionization, but there was also an air of mystery surrounding the wave of optimism that replaced the fearful, thrifty mindset of the Depression era. According to the cycle gang, it’s part of a nine-, eleven-, or maybe seventeen-year cycle, and who knows? They might be right.

This doesn’t go off-topic related to the inflation narrative. It stands to reason that the US economy differs greatly from all other economies for some reasons, such as the availability of finance, the entrepreneurial spirit, and the relative lack of regulations. Compared to other economies, it is more resilient and sturdy, with a larger percentage of small enterprises and independent contractors. While it’s not quite the same as “Go west, young man” and the cowboy mentality, it is far less conformist than in the UK and Europe.

In the US, anyone can set up shop and offer to paint your home. In Germany, obtaining a license is mandatory and comes with costs and lost time for “training.” There are 400 small firms worldwide, with 33.3% located in the United States. Astoundingly, Japan has a high percentage as well, but no one compares to the US, where 99.9% of all companies have fewer than 250 workers.

The decisions made by central banks also differ as a result of these distinctions. It’s just hooey to talk about “divergence” in central bank decision-making. Disinflation in all of the big economies is essentially the same. Because of their economies’ far slower growth rates, the BoE and ECB can consider reducing interest rates earlier than they would have to due to inflation. This implies a decrease in both the increase of employment and the consumer expenditure that fuels inflation.

As a result, the ECB will be less concerned about rate cuts in June when faced with the same data as the Fed, and it can be OK with the core at 2.7% minus something. Not quite apples and oranges, but close enough.

View the Reuters chart. As we stated in our writing from last Friday, one more tick higher might very well trigger an overreaction frenzy that extends the first cut out into the upcoming year or perhaps solidifies the notion of a raise. On the other hand, a nice decline would eliminate November and bring back the notion of a September reduction. Furthermore, we believe that a Nov cut is not possible for the reasons that follow.

One piece of information, whether or not it is significant to the Fed, can influence rates and the value of the dollar. This indicates that traders are apprehensive, if only because they are susceptible to what appears to be a switcheroo and lack a logical most-like scenario. For instance, the prospect that the Fed may hike rates sooner is bolstered by the fact that we will likely receive a revised estimate of GDP on Thursday. Once more, GDP is a background variable rather than a direct Fed driver.

Both headline and core PCE inflation are predicted to decline very little, if at all, with the core falling by a pitiful 0.1%. After the poor Q1 CPI figures, this is not significant enough to be called a trend reversal. Additionally, the ECB can make cuts while the US must wait if the eurozone maintains its 2.7% growth rate. It implies that there is something “wrong” with the way the dollar is weakening right now in terms of institutional and economic factors. Although the interpretation of facts can be incorrect, sentiment cannot. Now is the moment to exercise extreme caution and only accept modest offers from those with whom you are not infatuated.

justifications for rate cuts by the Fed

Don’t make the mistake of miscalculating inflation twice. Make the yield curve normal. Stop any signs of a recession. Mortgage rates can aid in housing. assist banks with commercial real estate loan rollovers.

Assist the financial market. Keep in sync with the ECB (as well as SNB and Riksbank). Assist the present administration or, if waiting until after the November election, steer clear of charges of political bias.

This is a small sample from the much longer “The Rockefeller Morning Briefing,” which has roughly ten pages. The Briefing is a daily publication that has been providing knowledgeable analysis and insight for more than 25 years. The paper provides extensive background information and is not meant to advise FX trading. For trading reasons, Rockefeller generates additional reports (in spot and futures).